Download the notebook here!

Interactive online version: ![]()

Optimization

[1]:

from functools import partial

from temfpy.optimization import carlberg

from scipy import optimize as opt

import matplotlib.pyplot as plt

from scipy.stats import norm

import seaborn as sns

import scipy as sp

import pandas as pd

import numpy as np

from optimization_problems import get_test_function_gradient

from optimization_problems import get_parameterization

from optimization_problems import get_test_function

from optimization_auxiliary import process_results

from optimization_auxiliary import get_bounds

from optimization_plots import plot_contour

from optimization_plots import plot_surf

from optimization_plots import plot_optima_example

from optimization_plots import plot_true_observed_example

Outline

Setup

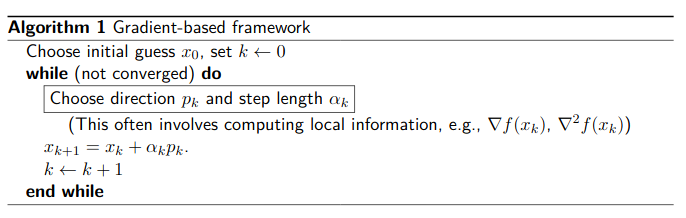

Algorithms

Gradient-based methods

Derivative-free methods

Benchmarking exercise

Special cases

Setup

In the finite-dimensional unconstrained optimization problem, one is given a function  and asked to find an

and asked to find an  such that

such that  for all

for all  . We call

. We call  the objective function and , if it exists, the global minimum of . We focus on minimum - to solve a minimization problem, simply minimize the negative of the objective.

the objective function and , if it exists, the global minimum of . We focus on minimum - to solve a minimization problem, simply minimize the negative of the objective.

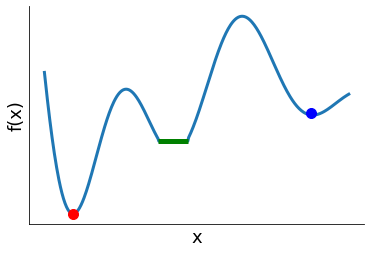

We say that  is a …

is a …

strict global minimum of

if  for all

for all  .

.weak local minimum of

if  for all in some neighborhood of .

for all in some neighborhood of .strict local minimum of

if  for all in some neighborhood of .

for all in some neighborhood of .

[2]:

plot_optima_example()

Let  be twice continuously differentiable.

be twice continuously differentiable.

First Order Necessary Conditions: If

is a local minimum of , then  .

.Second Order Necessary Condition: If

is a local minimum of , then  is negative semidefinite.

is negative semidefinite.

We say is a critical point of if it satisfies the first-order necessary condition.

Sufficient Condition: If

and

and  is negative definite, then is a strict local minimum of .

is negative definite, then is a strict local minimum of .Local-Global Theorem: If

is concave, and is a local minimum of , then is a global minimum of .

Key problem attributes

Convexity: convex vs. non-convex

Optimization-variable type: continuous vs. discrete

Constraints: unconstraint vs. constraint

Number of optimization variables: low-dimensional vs. high-dimensional

These attributes dictate:

ability to find solution

problem complexity and computing time

appropriate methods

relevant software

Always begin by categorizing your problem

Always begin by categorizing your problem

Optimization problems are ubiquitous in economics:

Government maximizes social welfare

Competitive equilibrium maximizes total surplus

Ordinary least squares estimator minimizes sum of squares

Maximum likelihood estimator maximizes likelihood function

Algorithms

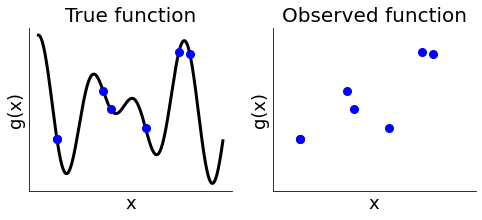

We are mostly blind to the function we are trying to minimize and can only compute the function at a limited number of points. Each evaluation is computationally expensive.

[3]:

plot_true_observed_example()

Goals

reasonable memory requirements

low failure rate, convergence conditions are met

convergence in a few iterations with low cost for each iteration

Catergorization

gradient-based vs. derivative-free

global vs. local

Question

How to compute derivatives?

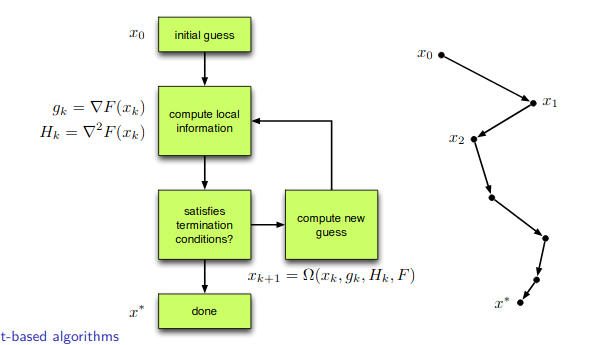

Gradient-based methods

Benefits

efficient for many variables

well-suited for smooth objective and constraint functions

Drawbacks

requires computing the gradient, potentially challenging and time-consuming

convergence is only local

not-well suited for noisy functions, derivative information flawed

Second derivative are also very useful, but …

Hessians are

, so expensive to construct and store

, so expensive to construct and storeoften only approximated using quasi-Newton methods

Questions

How to use gradient-based algorithms to find a global optimum?

Any ideas on how to reduce the memory requirements for a large Hessian?

There is two different classes of gradient-based algorithms.

Line-search methods

compute

be a descent direction

be a descent directioncompute

to produce a sufficient decrease in the objective function

to produce a sufficient decrease in the objective function

Let’s see here for how such a line search looks like in practice for the Newton-CG algorithm.

Trust-region methods

determine a maximum allowable step length (trust-region radius)

compute step

with

with  using a model

using a model

As an example implementation, see here for the scipy.optimize_trustregion.py implementation.

Derivative-Free Methods

Benefits

often better at finding a global minimum if function not convex

robust with respect to noise in criterion function

amenable to parallelization

Drawbacks

extremely slow convergence for high-dimensional problems

There are two different classes of derivative-free algorithms.

heuristic, inspired by nature

basin-hopping

evolutionary algorithms

direct search

directional

simplicial

Test function

![f(x) = \tfrac{1}{2}\sum_{i=1}^n a_i\cdot (x_i-1)^2+ b\cdot \left[ n-\sum_{i=1}^n\cos(2\pi(x_i-1))\right],](../../_images/math/3f249a97418d36813afac1603cf0e1b5c2fae993.png)

where  and

and  provide the parameterization of the function.

provide the parameterization of the function.

Exercises

Implement this test function.

Visualize the shape of our test function for the one-dimensional case.

What is the role of the parameters

and ?

and ?What is the functions global minimum?

[4]:

??get_test_function

[5]:

??get_parameterization

We want to be able to use our test function for different configurations of the challenges introduced by noise and ill-conditioning.

[6]:

add_noise, add_illco, x0 = False, False, [4.5, -1.5]

def get_problem(dimension, add_noise, add_illco, seed=123):

np.random.seed(seed)

a, b = get_parameterization(dimension, add_noise, add_illco)

get_test_function_p = partial(get_test_function, a=a, b=b)

get_test_function_gradient_p = partial(get_test_function_gradient, a=a, b=b)

return get_test_function_p, get_test_function_gradient_p

dimension = len(x0)

opt_test_function, opt_test_gradient = get_problem(dimension, add_noise, add_illco)

np.testing.assert_equal(opt_test_function([1, 1]), 0.0)

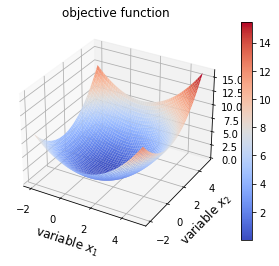

Let’s see how the surface and contour plots look like under different scenarios.

[7]:

opt_test_function, _ = get_problem(dimension, add_noise, add_illco)

plot_surf(opt_test_function)

/Users/emilyschwab/Desktop/IAME_Work/ose-course-scientific-computing/labs/optimization/optimization_plots.py:62: MatplotlibDeprecationWarning: Calling gca() with keyword arguments was deprecated in Matplotlib 3.4. Starting two minor releases later, gca() will take no keyword arguments. The gca() function should only be used to get the current axes, or if no axes exist, create new axes with default keyword arguments. To create a new axes with non-default arguments, use plt.axes() or plt.subplot().

ax = fig.gca(projection="3d")

Question

How is the global minimum affected by the addition of noise and ill-conditioning?

Benchmarking exercise

Let’s get our problem setting and initialize a container for our results. We will use the convenient interface to scipy.optimize.minimize. Its documentation also points you to research papers and textbooks where the details of the algorithms are discussed in more detail. We need to invest a little in the design of our setup first, but then we can run the benchmarking exercise with ease and even adding additional optimization algorithms is straightforward.

[8]:

ALGORITHMS = ["CG", "Newton-CG", "Nelder-Mead", "Diff-Evol"]

add_noise, add_illco, dimension = False, False, 2

[9]:

x0 = [4.5, -1.5]

opt_test_function, opt_test_gradient = get_problem(dimension, add_noise, add_illco)

df = pd.DataFrame(columns=["Iteration", "Distance"], index=ALGORITHMS)

df.index.name = "Method"

Let’s fix what will stay unchanged throughout.

[10]:

call_optimizer = partial(

opt.minimize,

fun=opt_test_function,

x0=x0,

jac=opt_test_gradient,

options={"disp": True, "return_all": True, "maxiter": 100000},

)

We prepared some functions to process results from the optimizer calls.

[11]:

??process_results

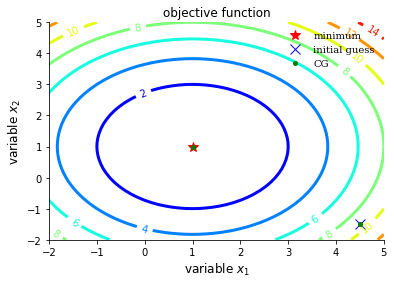

Conjugate gradient

[12]:

method = "CG"

res = call_optimizer(method=method)

initial_guess = [4.5, -1.5]

df = process_results(df, method, res)

plot_contour(opt_test_function, res["allvecs"], method, initial_guess)

Optimization terminated successfully.

Current function value: 0.000000

Iterations: 1

Function evaluations: 3

Gradient evaluations: 3

[12]:

<module 'matplotlib.pyplot' from '/Users/emilyschwab/miniconda3/envs/ose-course-scientific-computing/lib/python3.8/site-packages/matplotlib/pyplot.py'>

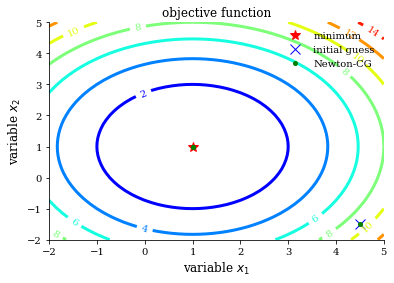

Newton-CG

[13]:

method = "Newton-CG"

res = call_optimizer(method=method)

initial_guess = [4.5, -1.5]

df = process_results(df, method, res)

plot_contour(opt_test_function, res["allvecs"], method, initial_guess)

Optimization terminated successfully.

Current function value: 0.000000

Iterations: 2

Function evaluations: 2

Gradient evaluations: 3

Hessian evaluations: 0

[13]:

<module 'matplotlib.pyplot' from '/Users/emilyschwab/miniconda3/envs/ose-course-scientific-computing/lib/python3.8/site-packages/matplotlib/pyplot.py'>

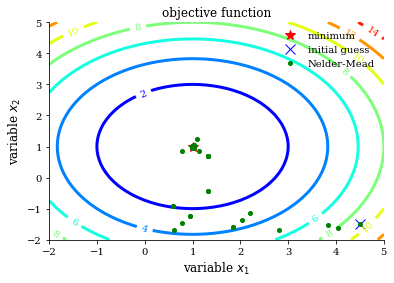

Nelder Mead

[14]:

method = "Nelder-Mead"

res = call_optimizer(method=method)

initial_guess = [4.5, -1.5]

df = process_results(df, method, res)

plot_contour(opt_test_function, res["allvecs"], method, initial_guess)

Optimization terminated successfully.

Current function value: 0.000000

Iterations: 51

Function evaluations: 95

/Users/emilyschwab/miniconda3/envs/ose-course-scientific-computing/lib/python3.8/site-packages/scipy/optimize/_minimize.py:522: RuntimeWarning: Method Nelder-Mead does not use gradient information (jac).

warn('Method %s does not use gradient information (jac).' % method,

[14]:

<module 'matplotlib.pyplot' from '/Users/emilyschwab/miniconda3/envs/ose-course-scientific-computing/lib/python3.8/site-packages/matplotlib/pyplot.py'>

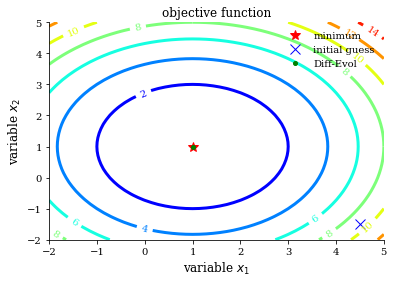

Differential evolution

[15]:

??get_bounds

[16]:

method = "Diff-Evol"

res = opt.differential_evolution(opt_test_function, get_bounds(dimension))

initial_guess = [4.5, -1.5]

plot_contour(opt_test_function, res["x"], method, initial_guess)

df = process_results(df, method, res)

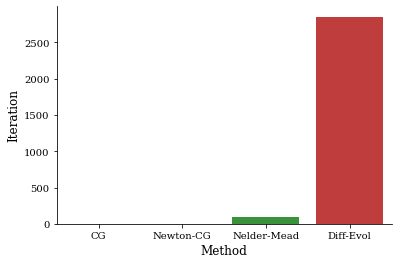

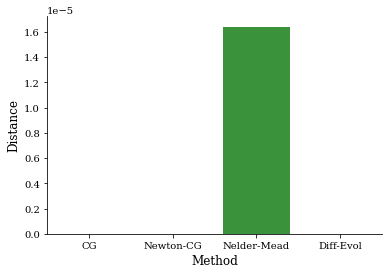

Summary

[17]:

_ = sns.barplot(x="Method", y="Iteration", data=df.reset_index())

[18]:

_ = sns.barplot(x="Method", y="Distance", data=df.reset_index())

Speeding up test function

We want to increase the dimensionality of our optimization problem going forward. Even in this easy setting, it is worth to re-write our objective function using numpy to ensure its speedy execution. A faster version is already available as part of the Python package temfpy. Below, we compare our test function to the temfpy version and assess their performance in regard to speed.

[19]:

??get_test_function

[20]:

??carlberg

It is very easy to introduce errors when speeding up your code as usually you face a trade-off between readability and performance. However, setting up a simple testing harness that simply compares the results between the slow, but readable, implementation and the fast one for numerous random test problems. For more automated, but random, testing see Hypothesis.

[21]:

def get_speed_test_problem():

add_illco, add_noise = np.random.choice([True, False], size=2)

dimension = np.random.randint(2, 100)

a, b = get_parameterization(dimension, add_noise, add_illco)

x0 = np.random.uniform(size=dimension)

return x0, a, b

Now we are ready to put our fears at ease.

[22]:

for _ in range(1000):

args = get_speed_test_problem()

stats = get_test_function(*args), carlberg(*args)

np.testing.assert_almost_equal(*stats)

Let’s see whether this was worth the effort for a small and a large problem using the %timeit magic function.

[23]:

dimension, add_noise, add_illco = 100, True, True

x0 = np.random.uniform(size=dimension)

a, b = get_parameterization(dimension, add_noise, add_illco)

[24]:

%timeit carlberg(x0, a, b)

51.6 µs ± 20.3 µs per loop (mean ± std. dev. of 7 runs, 10000 loops each)

[25]:

%timeit get_test_function(x0, a, b)

618 µs ± 198 µs per loop (mean ± std. dev. of 7 runs, 1000 loops each)

In this particular setting, there is no need to increase the performance even further. However, as a next step, check out numba, for even more flexibility in speeding up your code.

Exercises

Repeat the exercise in the case of noise in the criterion function and try to summarize your findings.

What additional problems arise as the dimensionality of the problem for a 100-dimensional problem? Make sure to use the fast implementation of the test function.

Special cases

Nonlinear least squares and maximum likelihood estimation have special structure that can be exploited to improve the approximation of the inverse Hessian.

Nonlinear least squares

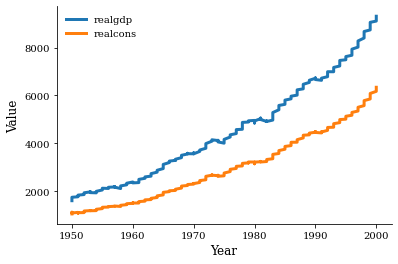

We will estimate the following nonlinear consumption function using data from Greene’s textbook:

which is estimated with quarterly data on real consumption and disposable income for the U.S. economy from 1950 to 2000.

[26]:

df = pd.read_pickle("material/data-consumption-function.pkl")

df.head()

[26]:

| realgdp | realcons | ||

|---|---|---|---|

| Year | qtr | ||

| 1950 | 1 | 1610.5 | 1058.9 |

| 2 | 1658.8 | 1075.9 | |

| 3 | 1723.0 | 1131.0 | |

| 4 | 1753.9 | 1097.6 | |

| 1951 | 1 | 1773.5 | 1122.8 |

Let’s confirm the basic relationship to get an idea of what to expect for the estimated parameters.

[27]:

fig, ax = plt.subplots()

x = df.index.get_level_values("Year")

for name in ["realgdp", "realcons"]:

y = df[name]

ax.plot(x, y, label=name)

ax.set_xlabel("Year")

ax.set_ylabel("Value")

ax.legend()

[27]:

<matplotlib.legend.Legend at 0x11dc95c70>

Now we set up the criterion function such that it fits the requirements.

[28]:

consumption = df["realcons"].values

income = df["realgdp"].values

def ssr(x, consumption, income):

alpha, beta, gamma = x

residuals = consumption - alpha - beta * income ** gamma

return residuals

ssr_partial = partial(ssr, consumption=consumption, income=income)

rslt = sp.optimize.least_squares(ssr_partial, [0, 0, 1])["x"]

Exercise

Evaluate the fit of the model.

Maximum likelihood estimation

Greene (2012) considers the following binary choice model.

![\begin{align*}

P[Grade = 1] = F(\beta_0 + \beta_1 GPA + \beta_2 TUCE + \beta_3 PSI)

\end{align*}](../../_images/math/bd0bf50aa315319ab351c036beee1701dba00b26.png)

where  the cumulative distribution function for either the normal distribution (Probit) or the logistic distribution (Logit).

the cumulative distribution function for either the normal distribution (Probit) or the logistic distribution (Logit).

[29]:

df = pd.read_pickle("material/data-graduation-prediction.pkl")

df.head()

[29]:

| GPA | TUCE | PSI | GRADE | INTERCEPT | GRADE | |

|---|---|---|---|---|---|---|

| OBS | ||||||

| 1 | 2.66 | 20 | 0 | 0 | 1 | 0 |

| 2 | 2.89 | 22 | 0 | 0 | 1 | 0 |

| 3 | 3.28 | 24 | 0 | 0 | 1 | 0 |

| 4 | 2.92 | 12 | 0 | 0 | 1 | 0 |

| 5 | 4.00 | 21 | 0 | 1 | 1 | 1 |

[30]:

def probit_model(beta, y, x):

F = norm.cdf(x @ beta)

fval = (y * np.log(F) + (1 - y) * np.log(1 - F)).sum()

return -fval

[31]:

x, y = df[["INTERCEPT", "GPA", "TUCE", "PSI"]], df["GRADE"]

rslt = opt.minimize(probit_model, [0.0] * 4, args=(y, x))

Exercise

Amend the code so that you can simply switch between estimating a Probit or Logit model.

Resources

Kevin T. Carlberg: https://kevintcarlberg.net

Software

SNOPT (Sparse Nonlinear OPTimizer): https://ccom.ucsd.edu/~optimizers/solvers/snopt

Gurobi https://www.gurobi.com

IBM CPLEX Optimizer https://www.ibm.com/analytics/cplex-optimizer

Books

Nocedal, J., & Wright, S. (2006). *Numerical optimization* . Springer Science & Business Media.

Boyd, S., Boyd, S. P., & Vandenberghe, L. (2004). *Convex optimization*. Cambridge university press.

Kochenderfer, M. J., & Wheeler, T. A. (2019). *Algorithms for optimization*. Mit Press.

Fletcher, R. (2000). *Practical methods of optimization (2nd edn)*. Wiley.

Nesterov, Y. (2018). *Lectures on convex optimization*. Springer Nature Switzerland.

Research

Moré, J. J., & Wild, S. M. (2009). Benchmarking derivative-free optimization algorithms. SIAM Journal on Optimization, 20(1), 172-191.

Beiranvand, V., Hare, W., & Lucet, Y. (2017). Best practices for comparing optimization algorithms. Optimization and Engineering, 18, 815–848.

Bartz-Beielstein, T., et al. (2020). Benchmarking in optimization: Best practice and open issues. arXiv preprint arXiv:2007.03488..